Risk is an essential consideration in all commercial transactions. Risk determines whether a transaction is viable, and risk is an indispensable – albeit often overlooked – component of the transaction's total price. In the Commonwealth context, risk management is a key component of the Commonwealth resource management framework.1

This briefing discusses how risk can be allocated and managed through the use of transactional documents such as contracts and leases, and in particular by a type of contractual clause known as an indemnity. It looks specifically at indemnities given by the Commonwealth (Commonwealth indemnities) and how they are regulated by the resource management framework before considering indemnities given by other parties to the Commonwealth (contractor indemnities) and the associated issue of liability caps.

In this issue

- Indemnities

- Indemnities create contigent liabilities

- Commonwealth indemnities in favour of a contractor

- Summary of the resource management framework

- Comcover considerations for Commonwealth indemnities

- Commonwealth indemnities tips

- Contractor indemnities and liability caps

- Liability caps checklist

- Summary

Indemnities

Terminology

In this briefing, 'risk' is used to mean the chance of something happening that may have an impact on objectives and potential costs. Risk is often specified in terms of events and consequences, and the magnitude of risk is normally determined by the combination of the consequences of an event and the likelihood of that event occurring.2

Another term for the consequence of a risk occurring is 'damage', which goes hand in hand with the legal responsibility for the damage, or 'liability'.3 Legal agreements such as contracts and deeds assign the liability for damage to one or more parties in the event that a specified risk occurs. An indemnity is a particular type of contractual clause that allocates liability between parties and is normally expressed in the form of one party 'indemnifying' another for a particular class or classes of liability.

In this briefing there is an assumption that the Commonwealth is dealing with a provider of goods or services, who will be referred to as the 'contractor'. The contractor could be anyone – it could be a landlord under a lease; a builder under a works contract; an IT provider; or a specialist consultant engaged by the entity to provide, for example, audit, accounting or legal services. It could be an outsourced payroll provider, a provider of travel services, a director of a Commonwealth authority or company or a supplier of goods to the Commonwealth. The discussion is equally applicable to all of these scenarios, but the single term 'contractor' is used for convenience. While this briefing primarily discusses indemnities in the context of procurement, much of the discussion will also be applicable to other types of contracts, including grants.

Sources of liability

Before examining indemnities in more detail, it is worth commenting on the general nature of contractual liability. One of the primary purposes of all legal agreements is to regulate liability (the other, related, purpose is to provide an agreed statement of the nature of the parties' relationship). It is obvious that, when a party enters into a contract, it is entering into a legally binding arrangement under which it can incur legal liability to the other contracting party for breach of that contract.

However, this does not mean that breach of contract is the only means by which a party may become liable, or that the potential scope of liability is limited to the clauses of the contract. For example, the Commonwealth can lease land from another person and then conduct an activity that is noisy and noxious and has an adverse effect on other tenants. This could be a breach of the lease, for which the Commonwealth would be liable to the landlord. But it could give rise to liability under other causes of action at the same time. It could also be the tort of nuisance or a breach of applicable environmental legislation.

Identifying all possible sources of potential liability is part of risk assessment and management generally. It is particularly relevant to indemnities. Being aware of the scope of potential liability assists greatly when considering the terms of proposed indemnities and determining whether they extend the Commonwealth's liability beyond that for which it would generally be liable (such as in negligence).

What is an indemnity?

At law, an indemnity is a legally binding promise by which one party undertakes to accept the risk of loss or damage another party may suffer. Essentially, it is a promise to 'hold harmless', and these exact words are often used in indemnity provisions, particularly older ones.

The classical form of indemnity is an insurance contract. Under an insurance contract, an insurer agrees to indemnify the policyholder in respect of certain specified losses and liabilities if certain specified events occur. In this case, the whole contract is one of indemnity.

The context of this briefing is contractual indemnities, which are a specific class of indemnity. A contractual indemnity is typically one provision of a larger commercial arrangement which states that a party agrees to hold harmless another party against the risk of loss or damage that that other party may suffer (including that party's liability to third parties for third party loss resulting from activities under the contract).

Indemnities create contingent liabilities

Where a contract does not explicitly allocate liability between the parties, each party's liability will be determined at general law on the facts of each event. To provide greater certainty and/or to shift liability that may have fallen on one party at general law to another party, a liability regime may be agreed and set out in the contract. To achieve this outcome, the regime may impose a contractual obligation to pay money if a specified event occurs (such as an indemnity). This is called a 'contingent liability' (that is, the liability to pay is contingent upon the event occurring).

Anatomy of an indemnity

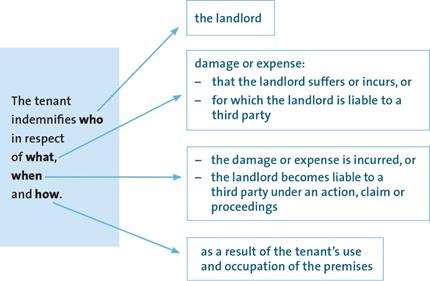

Invariably, an indemnity can be broken down into 4 constituent components: 'who', 'what', 'when' and 'how'.

Example

The landlord has requested the grant of an indemnity in the following terms:

The tenant indemnifies the landlord in respect of all actions, claims, proceedings, losses, costs, expenses and damages which the landlord suffers, incurs or becomes liable for and which arise from the tenant's use and occupation of the premises.

Who gets the benefit of the indemnity?

The first of the 4 elements is 'who'. This refers to the person that the tenant is indemnifying – in this case, the landlord. In the case of contractual indemnities, the 'who' will almost invariably be the other party to the contract, although sometimes the language used in the contract will be broad enough to extend the 'who' to also include officers, employees, agents, sub-contractors and, in some cases, related parties such as holding companies.

What types of liability does the indemnity cover?

The second element is 'what'. This refers to those things for which the indemnity is granted – in this case, 'all actions, claims, proceedings, losses, costs, expenses and damages'. These are fairly standard terms in an indemnity.

Clearly, there can be a range of different types of liability that might be picked up by this type of language, including liabilities for:

- tangible losses (for example, death and injury, damage to property)

- intangible losses (for example, infringement of intellectual property rights, damage to data, disclosure of personal or confidential information)

- pure economic losses (for example, statutory fines or penalties, lost productivity, loss of opportunity).

When is the indemnity applicable?

The third element is 'when'. In this case, it is those things 'which the landlord suffers, incurs or becomes liable for'. Note that it could have just said those losses, costs and so on 'that the landlord becomes liable for', which is much narrower than losses, costs and so on which the landlord suffers or incurs. This is because the use of the term 'liable' implies a legal obligation to pay (that is, there is no choice) whereas the term 'losses incurred' is broad enough to encompass voluntary expenditure incurred by the landlord in the absence of legal compulsion.

How is the indemnity triggered and what does it cover?

The fourth element is 'how'. It is the most important element of all because it is the trigger that invokes the indemnity. In this case, the trigger is all of those things 'which arise from the tenant's use and occupation of the premises'. This is extremely broad. This indemnity can be activated whether or not there is any fault on the part of the tenant.

A much narrower provision would be something like 'arising out of the negligence of the tenant'. This actually requires actionable negligence on the part of the tenant before the indemnity is triggered. Importantly, this form of indemnity, subject to one qualification, does not extend the tenant's exposure beyond that for which it would be liable, because the common law of negligence would apply in any event (this is especially significant in the context of Comcover insurance: see p 13).

Legal costs under indemnities

Even where an indemnity is triggered by the tenant's negligence and therefore seemingly goes no further than the common law, it can go further in the award of costs following a court case. Generally, after one side wins a court case it will be awarded costs, but the winning party does not usually get 100% of those costs. However, under this indemnity the landlord would be entitled to 100% of its legal costs. So, commercially, the indemnity does go a little further than the common law in that respect. But it does not expose the tenant to liabilities by way of additional causes of action.

Meaning of 'suffers or incurs'

In the case of the broader 'suffers or incurs' wording, though, the indemnity could result in the tenant incurring liability for which it would not otherwise have been liable. The expression 'arising out of the tenant's use and occupation' is broad enough to capture those things that are not actionable but which nevertheless cause the landlord loss. For example, if the tenant builds a structure on the land with the landlord's consent which blocks out the light and air flow to a neighbouring tenant and that neighbouring tenant successfully sues the landlord for derogating from the grant of its lease, the landlord may be able to recover the lost rent from the tenant, despite the landlord's earlier consent.

Proportionate liability legislation

The scope of the tenant's liability may also be affected by proportionate liability legislation in the relevant jurisdiction. Some jurisdictions (for example, Queensland) have proportionate liability regimes that cannot be contracted out of. This may mean that a party's liability is limited to its share of responsibility for another party's loss, irrespective of the form of indemnity contained in an agreement between those parties. As different proportionate liability legislation has been introduced in each jurisdiction, it is important to examine the regime applicable to the jurisdiction relevant to each individual contract.

Even standard form indemnities need careful consideration

Indemnities come in all shapes and sizes, although the wording (especially in similar classes of legal agreement) can be similar. Nonetheless, it is important to examine the terms of an indemnity before allowing its insertion into a contract, because seemingly innocuous indemnities have the potential to markedly increase risk exposure. Moreover, they are not necessarily labelled as indemnities in the contract.

An example is a clause that indemnifies a specialist contractor for all liability 'arising out of the provision of the specialist services'. The services are being provided for the entity and it has agreed to indemnify the specialist contractor for liability arising out of the provision of the services. However, its terms are arguably wide enough to cover acts of the contractor that are fraudulent, reckless or negligent. So, if the contractor was fraudulent and incurred liability because of that fraud, it could arguably seek recourse for the loss from the entity.

Commonwealth indemnities in favour of a contractor

In the sphere of Commonwealth contracting, Commonwealth indemnities are particularly significant because the legal, policy and resource management framework within which Australian Government entities enter into contracts gives specific recognition to, and has specific policies intended to deal with, Commonwealth indemnities.

Indemnities are considered from a number of different perspectives

In assessing an indemnity in the Commonwealth context, there are a number of relevant perspectives, all of which are closely related to each other:

- First, there is the commercial or financial perspective of an individual entity: what are the commercial or financial implications for the entity, acting on behalf of the Commonwealth, in granting an indemnity to a contractor in a particular contract? That is, what is the potential cost to the affected entity of this commitment requested by the contractor?

- Second, what are the implications of a proposed indemnity from a resource management framework perspective? This deals with the requirement to undertake a risk assessment, obtain approval under any applicable legislation and consider Commonwealth and departmental policies in approving proposed arrangements that contain contingent liabilities.

- Third, what are the implications of granting a proposed indemnity on the insurance coverage enjoyed by an Australian Government entity?

- Fourth, what are the implications of a proposed indemnity from a broader Commonwealth policy perspective? For example, is the indemnity contrary to other Australian Government policy, such as policy relating to particular industry sectors? A further consideration is whether it is likely to set an undesirable precedent.

- Fifth, what is the potential impact on the wider Commonwealth budget should an indemnity crystallise? Indemnities entered into by individual entities can affect the Commonwealth as a whole if their cost cannot be met from that entity's appropriations.

The second and third perspectives are discussed later in this briefing. It should be emphasised that the consequence of the first perspective is that a decision to grant an indemnity by the Commonwealth is a commercial or financial decision, not a legal decision, although an informed commercial or financial decision will often be made with the assistance of legal advice. This is not to say that the decision is a commercial or financial decision alone. Other perspectives, such as the Commonwealth policy framework applicable to indemnities, will impact on this decision.

Legislative and policy framework for Commonwealth indemnities

A complete description of the Commonwealth resource management framework is beyond the scope of this briefing. For this reason, the following discussion focuses on the key aspects of the resource management framework relevant to risk, liability and indemnities.

The resource management framework is underpinned by the Public Governance, Performance and Accountability Act 2013 (Cth) (PGPA Act), the Public Governance, Performance and Accountability Rule 2014 (Cth) (PGPA Rule), the Public Governance, Performance and Accountability (Finance Minister to Accountable Authorities of Non-Corporate Commonwealth Entities) Delegation 2014 (the Finance Minister's Delegation) and the Public Governance, Performance and Accountability (Financial Reporting) Rule 2015 (Financial Reporting Rule).

PGPA legislation

The PGPA Act provides the following:

- The accountable authority of an entity must govern the entity in a way that promotes 'proper use' of public resources and the financial sustainability of the entity (PGPA Act s 15), and in a way that is not inconsistent with the policies of the Commonwealth (PGPA Act s 21).

- Note that 'proper use' means efficient, effective, economical and ethical use that is not inconsistent with the policies of the Commonwealth (PGPA Act s 8).

- As part of an accountable authority's general duties, section 16 of the PGPA Act requires the accountable authority to establish and maintain appropriate systems of risk oversight and management for the entity, and an appropriate system of internal control for the entity. This includes by implementing measures directing at ensuring officials of the entity comply with 'the finance law' (which encompasses the PGPA Act, the PGPA Rule, any instrument made under the Act or an appropriation Act).

- The accountable authority of an entity is able to give instructions (called Accountable Authority's Instructions or AAIs) to officials in that entity on various matters relating to the finance law (PGPA Act s 20A(1)).

- An official must not enter into an arrangement under section 23(1) or approve a commitment of relevant money under section 23(3) unless the accountable authority has delegated them the power to do so (PGPA Act s 23 and s 110). An approval of a commitment of relevant money (whether done in the exercise of power under section 23(3) or as an inherent part of exercising a discretionary power to engage in expenditure under some other Act) must be recorded in accordance with the requirements of the PGPA Rule (PGPA Rule s 18).

- An 'arrangement' includes contracts, agreements, deeds or understandings (PGPA Act s 23(2)).

- If an accountable authority delegates powers under the PGPA Act to officials the accountable authority still needs to comply with its duty to promote the proper use and management of public resources. Some of the ways it may do this when the official is exercising the power is to impose conditions in the delegation (or give instructions) about the exercise of the power which the official must comply with. The official must also comply with his or her duties under sections 25 to 29 of the PGPA Act. In particular, sections 25 and 26 require the official to act with care and diligence, and for a proper purpose when exercising these powers.

- The Finance Minister is empowered to grant an indemnity, guarantee or warranty on behalf of the Commonwealth, provided that its terms comply with any requirements of the PGPA Rule4 (PGPA Act s 60).

- The Finance Minister can (with some exceptions) delegate any of their PGPA Act powers, functions or duties to an accountable authority in writing. The Finance Minister can also impose conditions on the exercise of those delegated powers (PGPA Act s 107).

- The accountable authority for an entity can (with some exceptions) delegate any of the powers, functions or duties conferred on them by the Finance Minister to an official of an entity. The accountable authority can also impose conditions on the exercise of those delegated powers and must impose the same conditions on the official as the Finance Minister imposed on the accountable authority (PGPA Act s 110).

- The Finance Minister may issue Commonwealth Procurement Rules (CPRs) and an official performing duties in relation to procurement must act in accordance with the CPRs (PGPA Act s 105B).

- The Finance Minister may issue Commonwealth Grants Rules and Guidelines (CGRGs) and an official performing duties in relation to grants administration must act in accordance with the CGRGs (PGPA Act s 105C).

Resource Management Guide No. 414

Resource Management Guides provide targeted guidance

Resource Management Guide No. 414: Indemnities, guarantees or warranties granted by the Commonwealth (RMG 414) was published in January 2015.

RMG 414 assists entities to comply with their obligations under the Commonwealth resource management framework in relation to granting indemnities, guarantees and warranties. It provides guidance about what is required for compliance under the finance law, in particular the Finance Minister's delegation under section 60 of the PGPA Act. It also suggests other matters to consider when contemplating the granting of an indemnity.

RMG 414 prescribes the same approach for indemnities, guarantees and warranties which cause a contingent liability to arise for an entity. Throughout RMG 414, each of these sources of contingent liability are referred to as 'indemnities'. Paragraph 8 of the RMG provides further detail on contingent liabilities and warranties that would not constitute an indemnity for PGPA Act purposes, such as:

- an agreement to reimburse a party for expenses incurred in the ordinary course of providing services

- a contractual warranty as to title or authority to enter into a transaction.

Paragraph 2 of RMG 414 reflects Direction 6.2 of the Finance Minister's Delegation, noting that, when granting an indemnity, 2 key principles must be considered:

- the risks should be borne by the party best placed to manage them

- benefits to the Commonwealth should outweigh the risks involved.

Significantly, RMG 414 emphasises that there should be an explicitly identified risk before an indemnity is granted.

RMG 414 also notes that the obligations of officials should be understood and undertaken proportionately to the scale and potential costs of the arrangement involving the indemnity. Officials must also consider any internal controls established by the accountable authority to align the process of granting an indemnity with the entity's appetite for risk and operating environment.

Relevant factors according to RMG 414

RMG 414 provides that, before granting an indemnity, officials must ensure:

- appropriate risk management arrangements have been implemented

- legislative requirements have been complied with.

According to RMG 414, when considering arrangements that involve granting an indemnity, the following factors should be considered:

- there is an explicitly identified risk

- time limits on the indemnity (for example, to claims made during the term of the contract)

- use by the contractor of commercial insurance

- reserving a termination right for the Commonwealth

- the imposition of maximum financial limits on claims

- the insertion of subrogation and notification clauses that give the Commonwealth the right to take over any litigation related to the indemnity.

There is no absolute prohibition on entities entering into indemnities without complying with this second list of pre-conditions (see p 10 of RMG 414).

There is also a recommendation that officials consider whether covering damage from acts by the indemnified person which are 'malicious, fraudulent, wilful, reckless etc' are appropriate from a policy perspective. This policy mirrors the Corporations Act 2001 (Cth), sections 199A–199C, and PGPA Rule section 23, which limit the circumstances in which Commonwealth companies and authorities may indemnify officers against their own conduct and insure them for liabilities arising out of that conduct.

RMG 414 also suggests officials consider whether, in the event that the indemnity was called upon, the most probable expense of the indemnity could be met by the entity's existing resources or by Comcover insurance.

Requirement to seek legal advice

RMG 414 contains a further recommendation that legal advice should be sought, where appropriate, to ensure that the Commonwealth is exposed to the minimum risk necessary to achieve the particular objective. The questions on which it is suggested that legal advice be sought are very comprehensive. They include:

- whether any applicable legislation restricts the power to enter into the arrangement

- what extra risks the Commonwealth would be accepting if it granted the indemnity

- whether the proposed indemnity only seeks to replicate liabilities imposed on the Commonwealth by common law or Commonwealth legislation – if so, as noted above, RMG 414 states that the provision is redundant and should be excluded unless there is a clear justification for the entity granting the indemnity (an entity may, for example, take the view that normal industry practice or likely additional costs constitute 'clear justifications').

Risk management under RMG 414

A persistent theme in RMG 414 is one of effective risk management. RMG 414 refers to the Commonwealth Risk Management Policy and much of the guidance either directly or implicitly contemplates that the risk identification and assessment process has been carried out. There are references to indemnities being granted in respect of 'explicitly identified risks'; to 'benefits to the Commonwealth... outweigh[ing] the risks involved'; to entities 'identifying risks to be managed' and 'analysing the risks'; to entities needing to 'rigorously investigate and identify' potential costs; and to appropriate risk management arrangements being in place.

All of these references assume appropriate risk assessment and management. RMG 414 provides a brief outline of appropriate risk management processes, but for more detail entities should consult AS/NZS ISO 31000:2009: Risk management – principles and guidelines.5

Commonwealth Procurement Rules

The CPRs make it clear that, as a general principle, risk should be borne by the party best placed to manage risk: an entity should not generally accept risks that another party is best placed to manage and should not seek to transfer to a contractor risks that the entity is best placed to manage. The CPRs also note that the extent of risk management will vary depending on the scale and complexity of the procurement. They emphasise that the systematic identification, analysis, treatment and allocation of risks must be built into an entity's procurement processes.

Finance Minister's Delegation – Direction 6.3

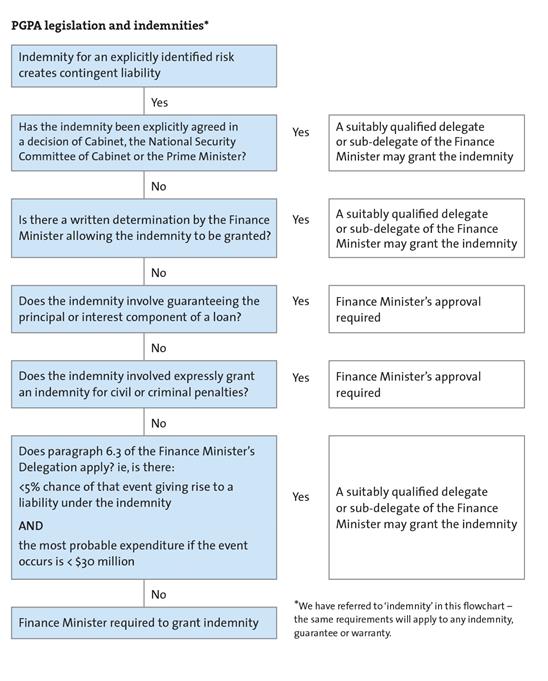

The Finance Minister's power under PGPA Act section 60 to grant an indemnity, guarantee or warranty has been delegated to the accountable authorities of entities, which are permitted to delegate the power in turn to officials. The Finance Minister's delegation to accountable authorities is subject to conditions, which must be imposed on any delegates of the accountable authority.

Direction 6.3 of the Finance Minister's Delegation empowers delegates to grant an indemnity, guarantee or warranty involving a contingent liability if the delegate is satisfied that:

- the likelihood of the event occurring is remote (less than 5% chance)

- the most probable expenditure that would need to be made in accordance with the arrangement, if the event occurred, would not be significant (less than $30 million).

If a proposed contingent liability does not fall within the above terms, the indemnity cannot be granted by the delegate and a request to approve the granting of the indemnity will need to be put to the Finance Minister. An exception to this is provided in Direction 6.4 of the delegation when a delegate may grant an indemnity where it has been explicitly agreed in a decision of Cabinet, the National Security Committee of Cabinet or the Prime Minister.

The power delegated under section 60 of the PGPA Act is further restricted in Direction 6.1 of the delegation in that the delegate cannot:

- grant a guarantee for the payment of any amount of principal or interest due on a loan

- grant an indemnity that would expressly meet the costs of civil or criminal penalties of the indemnified party.

For further information on the Finance Minister's Delegation see the diagram on p 12.

Sub-delegation

Accountable authorities may sub-delegate their power to grant indemnities reflecting the direction contained in Direction 6.3 of the Finance Minister's Delegation to an official in an entity. The sub-delegate is obliged to comply with any directions of the accountable authority when exercising the power; including those imposed by the Finance Minister in the Finance Minister's Delegation.

Officials contemplating granting an indemnity under a sub-delegation should also consult their AAIs for entity-specific guidance to sub-delegates and the scope of the sub-delegation. If necessary, legal advice should be sought as to whether the indemnity can be granted under the delegation.

Guidance from RMG 414 on Direction 6.3

RMG 414 contains guidance on dealing with the delegate's power under Direction 6.3 of the Finance Minister's Delegation. It states that:

- the availability of insurance to cover a particular contingent liability does not reduce the maximum expenditure that might be payable for Direction 6.3 purposes

- the potential proceeds of insurance must not be taken into account when determining, for Direction 6.3 purposes, the most probable expenditure that would need to be made in accordance with an arrangement containing a contingent liability.

Note that, when deciding what reasonable inquiries should be made to determine remoteness and materiality under Direction 6.3, it is important to note that delegates are required to undertake a 'proportionate inquiry'. This means that the scale of the investigation will be determined by the factors such as the complexity, level of risk and amount of the proposed contingent liability. For a contingent liability that is routine, simple, low-value and low-risk, a less extensive investigation may need to be undertaken.

Where an arrangement contains an uncapped contingent liability (for example, an uncapped indemnity from the Commonwealth), the most probable cost/expenditure may not be able to be calculated. This means that the second requirement for the exercise of power under Direction 6.3 of the Finance Minister's Delegation may not be able to be satisfied (the delegate cannot be satisfied that the maximum most probable expenditure associated with the contingent liability will be less than $30 million).

So, in the lease example used above on p 3, if the Commonwealth is the tenant giving the usual indemnity for the tenant's negligence, that indemnity, as standard and innocuous as it seems, is likely to trigger the need for the Finance Minister to grant the indemnity simply because it is by definition unquantifiable (i.e. uncapped).

However, an indemnity is not necessarily uncapped just because a financial limit is not expressly stated in the indemnity. A financial limit to the indemnity may be able to be calculated from the terms of the indemnity itself (for example, an indemnity for damage to specified property will be limited to the replacement value of that property). Where the indemnity contains a financial limit or where a financial limit can be calculated and the financial limit is under $30 million, a delegate may be able to grant the indemnity.

Requesting that the Finance Minister grant a Commonwealth indemnity, guarantee or warranty

If an indemnity, guarantee or warranty is not within the scope of Direction 6.3 of the Finance Minister's Delegation and none of the other exceptions discussed above apply, the written approval of the Finance Minister to grant the indemnity is required before the arrangement involving the indemnity is entered into.

RMG 414 explains that the Department of Finance has established a process through which the Finance Minister's approval to grant the indemnity contained in an arrangement should be sought.

Officials who have concluded that they need or may need the approval of the Finance Minister should liaise with their Agency Advice Unit (in Budget Group) within the Department of Finance. Officials should provide the unit with a copy of any:

- legal advice they have obtained on the arrangement involving the indemnity

- relevant risk assessment

- draft agreement or contract

- any other relevant document.

An entity's responsible Minister should also write to the Finance Minister:

- requesting that the indemnity in question be provided

- explaining why the entity cannot grant the indemnity under the Finance Minister's Delegation

- enclosing a copy of the Indemnity Grant Request Form, which is Attachment A to RMG 414.

The letter may contain some explanation for why the granting of the indemnity should be approved.

The Finance Minister will reply by letter to the responsible Minister for the entity, either approving or not approving the granting of the proposed indemnity. If the Finance Minister approves granting the indemnity, this will constitute authority for the specific indemnity for which approval was sought, following which the delegate within the entity can grant the indemnity by entering the relevant arrangement.

Where approval from the Finance Minister will be required, entities should consider the time frame and procedural steps required to obtain such an agreement in developing their procurement timetable and strategy.

Specific guidance to an entity's officials on resource management can be provided by the AAIs issued by the entity's accountable authority under PGPA Act section 20A. AAIs are legally binding upon the officials of that entity under the PGPA Act.

To assist entities in developing their own AAIs, the Department of Finance has issued Model AAIs. The Model AAIs contain a section on contingent liabilities (including indemnities). The Model AAIs should be used in conjunction with Resource Management Tool No. 206: Accountable Authority Instructions – Non-corporate Commonwealth entities.

Although they are entity-specific, in terms of providing guidance and instruction to officials on Commonwealth procurement policies and practice (including managing risk), AAIs largely encapsulate and expand upon the PGPA legislation, CPRs, CGRGs and relevant Finance guidance.

Summary of the resource management framework

The combined effect of the requirements of the resource management framework and relevant Commonwealth policies is that entities that are requested to provide an indemnity to another party should do the following:

- Carry out a risk assessment to determine whether an indemnity should be provided. The type and complexity of the assessment should be commensurate with the arrangement/s.

- Apply the principle that the party best placed to manage a risk should be responsible for that risk.

- Consider whether benefits (financial or otherwise) sufficiently outweigh the risk that the Commonwealth would be assuming.

- If an indemnity is to be granted, seek to limit any potential liability under the indemnity (for example, by including financial caps and time limits) where appropriate.

- Seek appropriate approvals before entering into an indemnity and meet all reporting and disclosure requirements.

- Actively manage the risks associated with the indemnity through development and implementation of a risk management plan to reduce the likelihood of it being called upon.

Comcover considerations for Commonwealth indemnities

It is beyond the scope of this briefing to comprehensively discuss the relationship between risk management and insurance. However, that relationship is obviously an aspect of risk management. Comcover is the Australian Government's general insurance fund.

Many contingent liabilities are uninsurable by nature, but entities need to have regard to those risks that are insurable risks in accordance with Comcover's policy terms and conditions. It should be noted that Comcover, as part of its risk management services, provides advice to Commonwealth entities on how to effectively manage risks and assists in seeking to instil a proper risk management culture via education programs and regular risk assessments. On 1 July 2014, Comcover released the Commonwealth Risk Management Policy.6

From a practical perspective, entities that intend to provide indemnities should be aware of Comcover Statement of Cover condition 19(3), which excludes from coverage 'liability arising out of any indemnity unless the liability would have arisen in the absence of such indemnity'. In other words, Comcover does not cover any liability under an indemnity beyond that for which an entity would have otherwise been liable, unless specific approval is obtained from Comcover beforehand. One consideration for whether coverage will be granted is whether the government policy on issuing and managing indemnities has been complied with (see Comcover Statement of Cover condition 4(3))

The Comcover Statement of Cover provides that the exclusion of indemnities from its coverage does not apply where government policy has been adhered to. The exception applies to indemnities where:7

- the entity has complied with applicable Australian Government policies on issuing and managing indemnities

- after making reasonable inquiries, the entity assessed:

- the likelihood of the event triggering the indemnity occurring is less than 5%

- the maximum probable expenditure if the event triggering the indemnity occurs is $5 million.

Note that there is also an exception for indemnities entered into before 1 July 2004.

As noted above, an adequate assessment of whether an indemnity does go beyond (rather than merely restates) the common law position requires an understanding that liability can arise from different sources (and not just breach of contract).

It should be noted that the presence of insurance, whether through Comcover or a commercial insurer, cannot be taken into account in determining the maximum amount payable for the purposes of granting the indemnity under Direction 6.3 of the Finance Minister's Delegation or in determining the most probable expenditure for the purposes of a sub-delegation under Direction 6.3 of the Finance Minister's Delegation.8

Commonwealth indemnities tips

- The decision to grant an indemnity must be informed by an entity's commercial objectives and wider Commonwealth policy objectives.

- Consider the wording of an indemnity carefully, even if it is a standard form indemnity, as small changes to wording can make a big difference to liability.

- Assess the risks.

- Discuss any proposed Commonwealth indemnity with Comcover.

- Where an indemnity is included as part of a Commonwealth contract, consider the requirements of both PGPA Act s 23and s 60.

- Finance has published a Resource Management Guide for granting and managing indemnities that should be considered prior to granting the indemnity. Under this Resource Management Guide, amongst other matters, officials should consider seeking to limit any potential liability (for example, by including financial caps and time limits) where appropriate.

- Where granting a proposed indemnity is outside the scope of the directions to delegates in the Finance Minister's Delegation, written approval from the Finance Minister to grant the indemnity will be required. Take this into account in planning the procurement/contracting process.

Contractor indemnities and liability caps

This briefing has so far looked at the Commonwealth's liability to the contractor, particularly where the Commonwealth grants an indemnity to the contractor. In this section we look at the contractor's liability to the Commonwealth.

As a result of its activities under the contract, the contractor may be liable to the Commonwealth for loss, damage or expense that the Commonwealth has suffered directly (for example, for damage to Commonwealth property) or indirectly (for example, for claims by third parties against the Commonwealth for third party loss as a result of the contractor's actions).

Commonwealth contracts often contain an indemnity from the contractor to the Commonwealth. The principles discussed above about the 'who', 'what', 'when' and 'how' of indemnities (see p 3–4) are equally relevant to indemnities provided by contractors.

What is a liability cap?

One of the most common issues that arises in relation to a contractor's liability to the Commonwealth is the issue of liability caps. A liability cap is a contractual provision that caps the liability of one contracting party to the other contracting party under the contract to a certain amount.

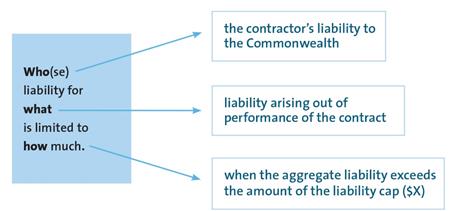

Anatomy of a liability cap

A useful way of looking at liability caps is to break them down into the following 3 components: 'who', 'what', and 'how (much)'.

Example

A contractor requests a liability cap in the following terms:

Who gets the benefit of the liability cap?

A liability cap benefits the party whose liability is being capped, which in this case is the contractor. For liabilities covered by the cap, the contractor's liability to the Commonwealth will be limited to the amount of the cap. The Commonwealth will bear the risk for all amounts above the amount of the cap.

What does the liability cap cover?

This refers to the types of liability covered by the liability cap. In this case, the liability cap is very broad and does not restrict the types of liability covered, provided that they arise out of performance of the contract. This could include claims for breach of contract, negligence or statutory claims. Note also that, unless the liability cap is linked to the contract in some way, the cap may be taken to apply to liabilities the contractor has to the Commonwealth that have nothing to do with the contract.

In most cases, the liability cap will be drafted so as to exclude certain liabilities for which the contractor is to retain unlimited liability.

It is important to consider the relationship between the liability cap and other provisions of the contract. For example, a liability cap in one part of the contract may limit an indemnity contained in another part of the contract.

Liability caps sometimes limit or exclude liability for 'indirect' or 'consequential' loss. Terms such as 'direct' and 'indirect' or 'consequential' loss may lead to uncertainty and it is often preferable to 'spell out' the exact types of losses intended to be excluded. There is case law which indicates that the term 'consequential loss' is likely to cover 'everything beyond the normal measure of damages, such as profits lost or expenses incurred through breach'.9

How much: i.e. how should the liability cap be set?

The liability cap will apply where the amount of the contractor's liability exceeds the amount of the cap. In this case, the amount of the liability cap is $X. As the clause provides that this is the 'aggregate liability' of the contractor, $X is the total amount that the contractor will be liable to the Commonwealth for liabilities that are covered by the cap. Liability caps can also be made to apply on a per-event basis or on an aggregate basis over a certain period of time. Sometimes the parties agree to both a per-event cap and an aggregate cap.

Liability caps are usually triggered when the party whose liability is being capped incurs a liability to the other contracting party in relation to the contract. In this case, the cap is triggered by liabilities of the contractor to the Commonwealth 'arising out of the contractor's performance of the contract'.

Another type of cap that should be avoided is one that caps liability to what the contractor can recover from insurance. This type of cap is fraught with difficulty because it is likely to be reliant on:

- the detailed terms and conditions of the contractor's insurance policy (and, in particular, it is subject to any exclusions set out in the policy)

- the contractor actually complying with the requirements of the policy so as not to void the insurance.

The resource management framework and Commonwealth guidelines and policies

Like all provisions of the contract, a liability cap will need to be considered in the context of entering an arrangement, such as under PGPA Act section 23(1). In some cases, it will also need to be granted under PGPA Act section 60. There are a number of Commonwealth policies and guidelines to consider in relation to liability caps.

Liability caps in information and communications technology contracts

Both the CPRs and RMG 414 provide that risks should generally be borne by the party best placed to manage them. RMG 414 also refers to A guide to limiting supplier liability in ICT contracts with Australian Government agencies, third edition, May 2013, published by the Department of Industry, which provides guidance on liability risk assessments for IT contracts.

This principle would dictate that, in general, where a contractor is better placed to manage the risk associated with its provision of goods or services to the Commonwealth, the contractor's liability to the Commonwealth in respect of that risk should not be limited by contract.

Do liability caps trigger the need for PGPA Act s 60 approval?

Whether a liability cap triggers the need for granting under PGPA Act section 60depends on the kinds of liability limited by the cap.10

A liability cap may result in the creation of a contingent liability if it creates an obligation to pay. According to RMG 414, arrangements containing the following types of liability cap will be regarded as contingent liabilities and will generally require to be granted under PGPA Act section 60 (either after approval to grant is given by the Finance Minister or by an appropriate delegate or sub-delegate where the granting is within the scope of the directions of the Finance Minister's delegation of power under s 60 PGPA Act):

- liability caps limiting a contractor's liability to a third party so that the Commonwealth is liable to the third party for any excess above that cap

- liability caps limiting a contractor's exposure for damage the contractor has itself suffered so that the Commonwealth is liable to the contractor for any excess.

Arrangements containing the following types of liability cap will not be regarded as contingent liabilities:

- liability caps limiting a contractor's liability to the Commonwealth for damage it directly causes to the Commonwealth

- liability caps limiting a contractor's liability to the Commonwealth so the Commonwealth cannot recover damages from the contractor if the Commonwealth is sued by a third party.

In other words, if a liability cap only limits a contractor's liability to the Commonwealth for damage that the contractor directly causes to the Commonwealth, the Commonwealth's guidance is that the liability cap will not, of itself, result in a need to grant it under PGPA Act section 60. Conversely, if the liability cap is more in the nature of an indemnity to the contractor, the indemnity will need to be granted under PGPA Act section 60(either by the Finance Minister or an appropriate delegate or sub-delegate).

For the circumstances where a delegate or sub-delegate may grant an indemnity under the Finance Minister's delegation of power under PGPA Act section 60, see p 10.

Comcover considerations for liability caps

Entities should also be aware that the Comcover Statement of Cover provides for Comcover to be subrogated to the rights of the entity when a claim for payment is made. It may be a breach of the policy to agree to a proposed liability cap without disclosing that fact to Comcover under condition 19(2)(d) on the basis that the entity has 'otherwise compromised [the entity's] legal position'. This may entitle Comcover to refuse to indemnify the entity. AGS sought clarification from Comcover on this issue, and Comcover's reply was as follows:

It must be stressed that the decision to include a liability cap within a contract is entirely the responsibility of the [entity] involved. There is no requirement to obtain Comcover approval for liability caps. However, if the liability cap relates to an insurable risk and the [entity] wishes Comcover to fund potential losses arising out[side] of the cap, then approval must be sought for Comcover's agreement to waive its right of subrogation. This approval must be sought in advance and provided in writing.

Liability caps for damage to other entities' property

There are some additional considerations for entities if they are considering capping a contractor's liability for damage to Commonwealth property that is not the responsibility of the entity. Section 15of the PGPA Act states that the accountable authority for an entity must manage the affairs of the entity in a way that promotes the proper use (being the efficient, effective, economical and ethical use) of Commonwealth resources for which the accountable authority is responsible. Therefore, when determining whether there is sufficient justification to issue a liability cap that limits a contractor's liability for damage to Commonwealth property for which that accountable authority is not responsible, the Department of Finance advises that the risk assessment should consider the impact on other entities.

If the liability cap is likely to affect a small number of entities, the accountable authority should consider consulting with those entities. If the liability cap is likely to affect all entities, the accountable authority should consider consulting with Finance.

This is in addition to any requirements under the PGPA Act, such as section 21, that an arrangement must not be entered into unless, among other things, it is not inconsistent with the policies of the Commonwealth.

In addition, an entity's Comcover cover relates to the insurable risks for which that entity is responsible. If a proposed liability cap relates to insurable risks for which another entity is responsible then Comcover may need to consult that entity. This can arise where a liability cap is expressed to encompass damage to Commonwealth property and, in the circumstances of the particular contract, there is a potential for the contractor to cause damage to Commonwealth property administered by more than one Commonwealth entity.

Contractor insurance considerations

This briefing does not look in any detail at commercial insurance, which is a substantial area in its own right. However, entities should be aware that, in the context of Commonwealth contracts, the primary purpose of requiring the contractor to hold commercial insurance in relation to particular liabilities is to ensure that the contractor will have the necessary resources to meet any liabilities that arise as a result of the contract. Entities should bear in mind the following:

- The fact that a person is required to hold insurance for a particular type of liability does not of itself make them liable for that type of liability. The common law, legislation or the terms of the contract will determine if that liability exists.

- Agreement to a certain level of insurance does not generally equate to agreement to limit liability to that level. Entities need to take care to avoid any misunderstandings about this issue.

- Commercial insurance policies often contain a range of terms and conditions that can impact on whether or not a claim may be made in particular circumstances. This can have a significant bearing on the effectiveness of the policy.

- In more complex, high-risk arrangements, it is necessary to obtain specialist insurance advice on proposed insurance arrangements for contractors.

Liability caps checklist

- As with indemnities:

- Some liability caps operate like indemnities and these are treated under the resource management framework in a similar way to indemnities (for example, they may require to be granted as indemnities under PGPA Act s 60).

- Assess the risks: this may include potentially undertaking a risk assessment and, if necessary, implementing a risk management plan.

- Remember that risk should generally be borne by the party best placed to manage the risk.

- The decision whether to agree to a liability cap must be informed by an entity's commercial objectives and wider Commonwealth policy objectives.

- Where a liability cap affects more than one entity, it may be prudent to discuss it with other affected entities or the Department of Finance.

- It is prudent to discuss liability caps with Comcover.

- Take care with the relationship between contractor indemnities, liability caps and contractor insurance.

Summary

The main points in this briefing are as follows:

- The decision to provide a Commonwealth indemnity or a cap on contractor liability is not a legal decision, although it will often need to be informed by sound legal advice.

- Risks should be allocated to the party best placed to manage them.

- In carrying out indemnity risk assessments, entities should consider the anatomy of the indemnity by reference to the 4-step analysis ('who', 'what', 'when' and 'how') described on p 3–4.

- Read and apply the Department of Finance's guidance in RMG 414, particularly regarding when a Commonwealth indemnity may be granted, the conditions that should be considered and when to seek legal advice.

- Some Commonwealth liability caps trigger the need for PGPA Act s 60 approval.

- In some cases, PGPA Act s 60 approval can be sought from within the entity under the Finance Minister's Delegation, but, in other cases, it may need to be sought from the Finance Minister.

- Liability caps that create a contingent liability are treated in a similar way to indemnities under the resource management framework.

- Finally, and most importantly, whether one is dealing with the legal, commercial, insurance or financial aspects of liabilities and indemnities, a risk assessment is important.

Notes

1 This briefing uses 'entities' to refer to non-corporate Commonwealth entities under the Public Governance, Performance and Accountability Act 2013 (PGPA Act).However, much of the discussion is also applicable to corporate Commonwealth entities under the PGPA Act in that it represents a prudent approach to the question of risk management.

2 Standards Australia, Australian/New Zealand Standard AS/NZS ISO 31000:2009: Risk management – principles and guidelines.

3 This briefing uses the word 'damage' – which implies a negative consequence – because this is the type of risk that is most often managed contractually. For completeness, note that AS/NZS ISO 31000:2009 defines 'risk' to include events that have both positive and negative outcomes. These positive (and less often analysed) risks are often referred to as 'opportunities'.

4 As of May 2015, there are no PGPA Rules specifically relating to s 60 of the PGPA Act.

5 See also the Commonwealth Risk Management Policy

6 Commonwealth Risk Management Policy

7 Note that RMG 414 indicates that insurance may not be taken into account in determining the most probable expenditure.

8 See condition 19(3) of the Comcover Statement of Cover [PDF].

9 Environmental Systems Pty Ltd v Peerless Holdings Pty Ltd [2008] VSCA 26at [93] per Nettle J. This position was followed in Allianz v Waterbrook [2009] NSWCA 224 and Alstom Ltd v Yokogawa Australia Pty Ltd (No 7) [2012] SASC 49.

10 See RMG 414.

This briefing is based on the 2006 Legal briefing no. 79: Indemnities in Commonwealth contracting (by Linda Richardson, Andrew Miles and Shaun Tipson) and an updated version, published as Legal briefing no. 86 in August 2010 (by Linda Richardson, Paul Lang and Cathy Reid), again updated and published as Legal briefing no. 93 in August 2011 (by Linda Richardson, Paul Lang and Cathy Reid) and again in 2015 (by Linda Richardson, Stuart Hilton and Jack Simpson).

Linda Richardson PSM is the General Counsel Commercial of AGS Commercial and has extensive expertise in commercial work, specifically government tendering and contracting and Commonwealth accountability. She has significant experience as a negotiator of commercial and government-to-government agreements, has drafted best practice guidance for various agencies on conducting liability risk assessments.

Paul Lang is a Deputy General Counsel in AGS Commercial. He has advised the Australian Government in many significant and complex commercial projects. He has an extensive background in public sector procurement, tendering and contracting, probity and process advice, privatisation, corporatisation, outsourcing, and grants and funding agreements.

Cathy Reid is a Deputy General Counsel in AGS Commercial and has advised government on a wide range of procurement and privatisation projects involving negotiation of complex risk allocation and management issues such as indemnities and liability caps.

© AGS All rights reserved

ISSN 1448-4803 (Print)

ISSN 2204-6283 (Online)

Important: This material is not professional legal advice to any person on any matter. It should not be relied upon without checking. The material is provided to clients for information only. AGS is not responsible for the currency or accuracy of the content of external website links referred to within this material. Please contact AGS before any action or decision is taken on the basis of any of the material in this message.

Contacts

Chief Counsel Commercial

Senior Executive Lawyer

Senior Lawyer